Policy Points

18.12.2009

Policy Points

A round-up of policy reports from the week ending on 12/18:

18.12.2009

Policy Points

The November jobs report released today by the Employment Security Commission offers little proof that a labor market recovery is underway.

Last month, North Carolina employers eliminated 8,800 more positions than they added with private-sector employers responsible for almost all of the losses (-8,500 positions). Although the state’s labor market has alternated between periods of slight payroll gains and modest losses over the last four months, the fundamental reality is that North Carolina’s labor market is stuck in place.

In November, North Carolina employers shed 8,800 more positions than they added. The public sector lost, on net, 300 positions, and the private sector cut, on net, 8,500 positions. Among private industries, leisure and hospitality services eliminated the most positions (-4,800), followed by manufacturing (-3,900) and trade, transportation and warehousing (-1,000). Education and health services posted the largest numerical gain (+1,900), followed by construction (+800). Additionally, a downward revision to the October report led to the net loss of another 3,100 positions.

The consequences of widespread joblessness are reflected in November’s household data. Last month, the labor force grew slightly due to new entrants and the return of some discouraged workers. Nevertheless, the share of the population participating in the labor force held steady. Additionally, North Carolina saw the unemployment rate (10.8 percent) and number of unemployed individuals (487,631) remain fairly constant between October and November.

Click here to read South by North Strategies’ full analysis of the latest employment report.

18.12.2009

Policy Points

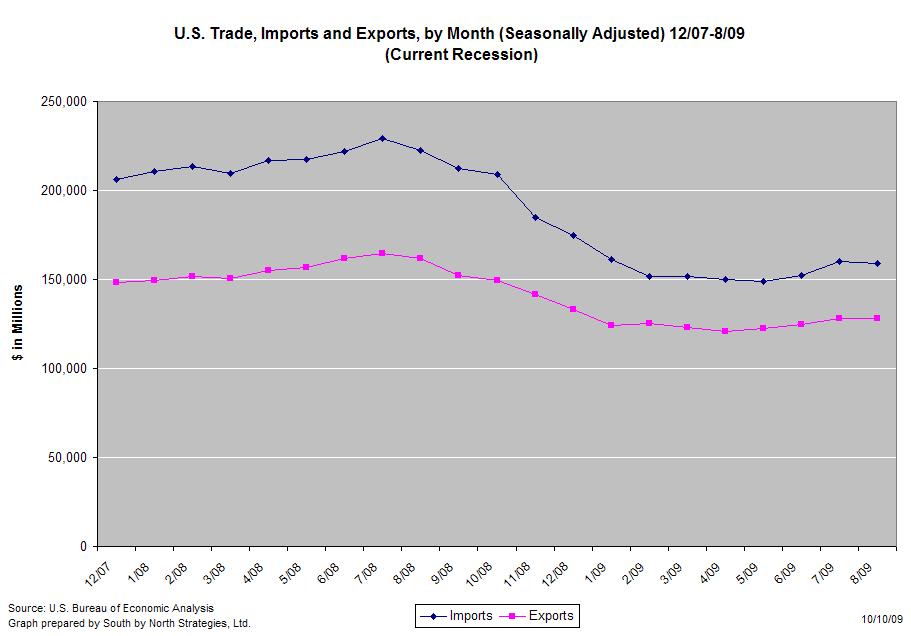

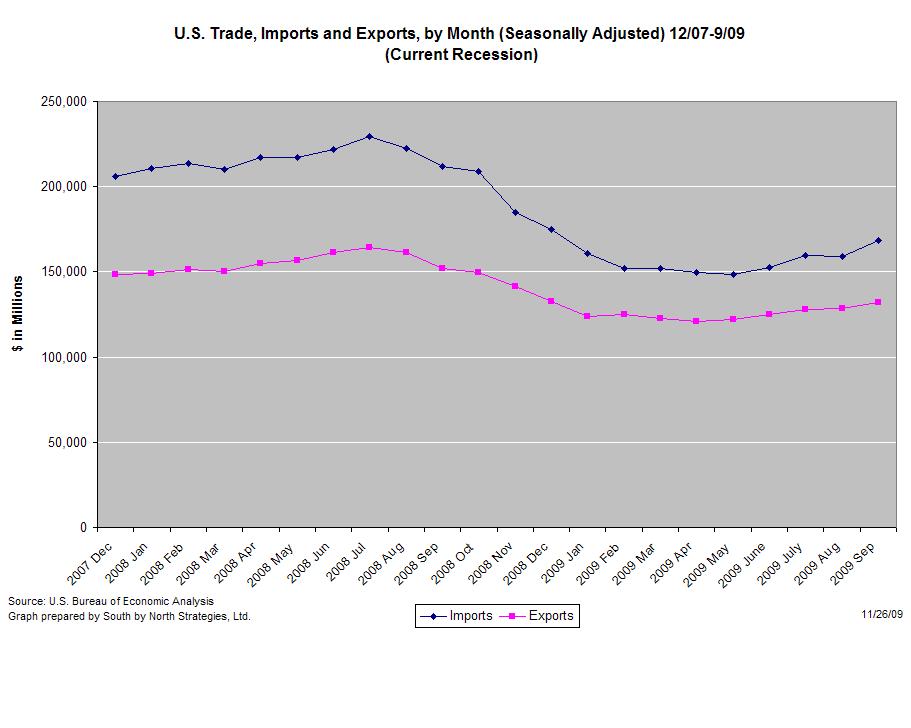

In October, the United States imported more goods and services from abroad than it exported, according to the most recent report from the Bureau of Economic Analysis. Compared to the revised September data, the October trade deficit was lower and the levels of of both imports and exports were higher

The graph (left) shows the changes in American imports and exports that have occurred since the start of the recession in December 2007.

The graph (left) shows the changes in American imports and exports that have occurred since the start of the recession in December 2007.

The recession has reduced American demand for foreign goods and services and foreign demand for American goods and services (though the fall in the dollar’s value likely is boosting American exports).

Compared to a year ago (seasonally adjusted), U.S. imports were 18.8 percent lower while exports were 8.6 percent lower. In recent months, both imports and exports have been trending upwards.

The rapid decline in imports has helped to reduce the trade gap. Last month, the U.S. imported $32.9 billion more than it exported  . When imports of petroleum products are excluded, the trade gap was $13.3 billion.

. When imports of petroleum products are excluded, the trade gap was $13.3 billion.

Compared to one year ago (seasonally adjusted), the non-petroleum trade deficit is 44 percent lower and the overall trade deficit is 44.5 percent lower.

17.12.2009

Policy Points

Economic policy reports, blog postings, and media stories of interest:

17.12.2009

Policy Points

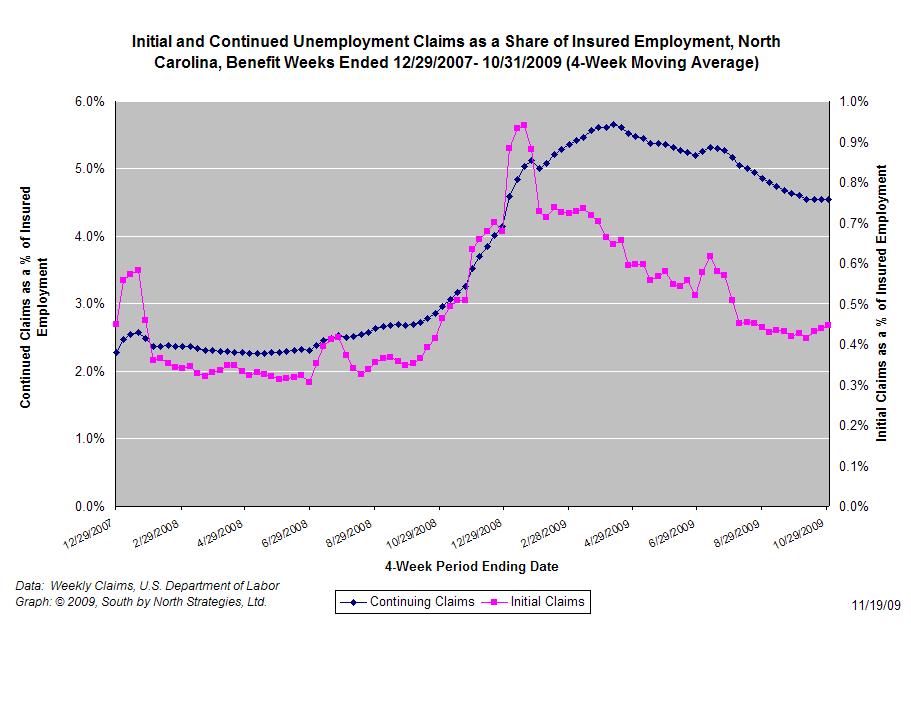

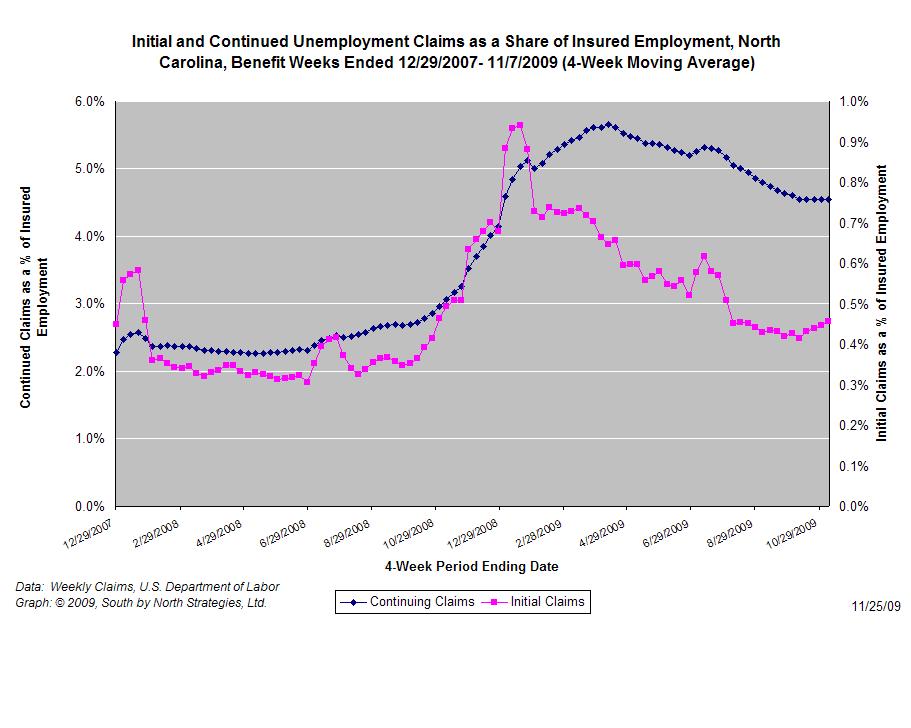

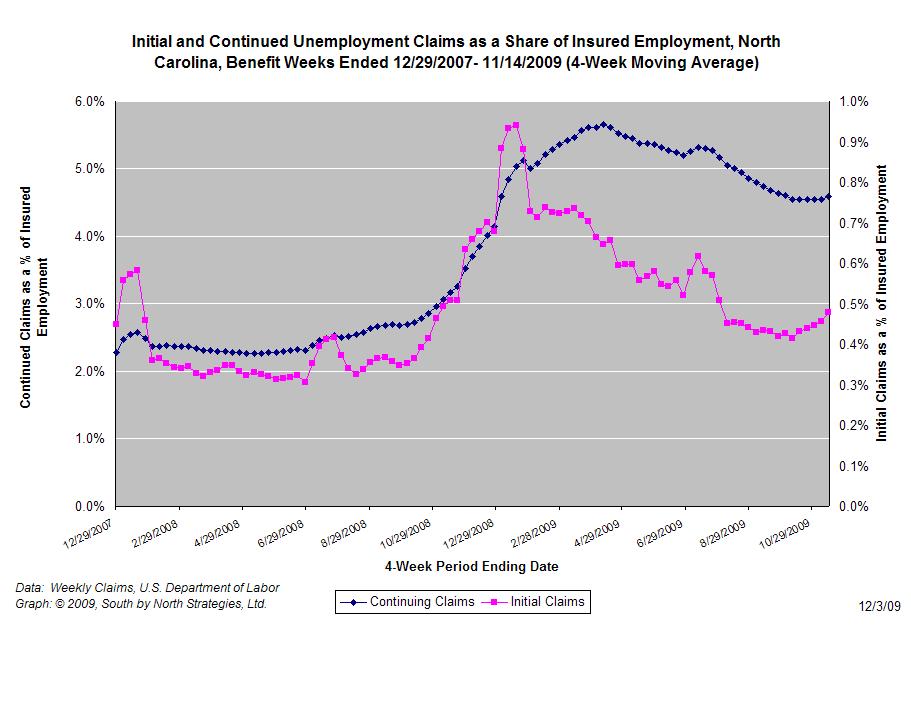

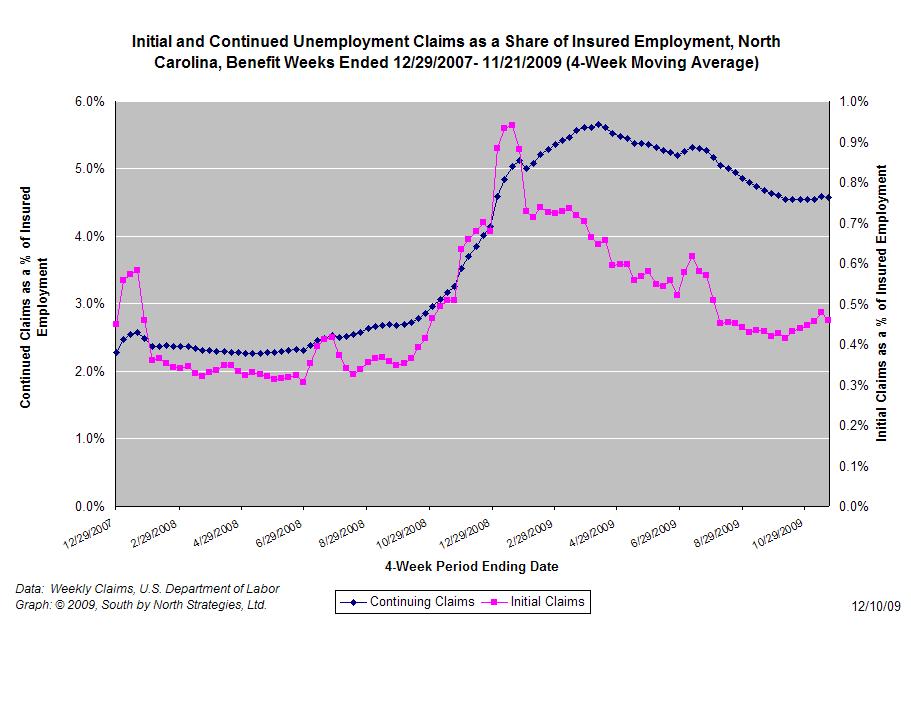

For the benefit week ending on November 28th, 32,368 North Carolinians filed initial claims for unemployment insurance, and 205,541 individuals applied for continuing insurance benefits. Compared to the prior week, there were many more initial and continuing claims; however, this is partly due to the fact that the previous filing week contained just three workdays owing to the Thanksgiving holiday. These figures come from data released today by the U.S. Department of Labor.

Averaging new and continuing claims over a four-week period — a process that helps adjust for seasonal fluctuations and better illustrates trends — shows that an average of 21,540 initial claims were filed over the last four weeks, along with an average of 187,405 continuing claims. Compared to the previous four-week period, both initial and continuing claims were higher.

One year ago, the four-week average for initial claims stood at 25,462 and the four-week average of continuing claims equaled 141,601.

The graph (right) shows the changes in unemployment insurance claims (as a share of covered employment) in North Carolina since the recession’s start in December 2007.

Although new and continuing claims appear to have peaked for this business cycle, the claims levels remain elevated and point to a labor market that remains extremely weak. Especially troubling is the high level of continuing claims, which suggests that unemployed individuals are finding it extremely difficult to find new positions.

Email Sign-Up

Email Sign-Up{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}